US DOMESTIC CONTENT SOLAR PANELS

Domestic content 101: Understanding bonus credit requirements

While many solar farm developers and EPCs in our industry are aware of the domestic content bonus, they may not be aware that US manufactured solar panels can meet this requirement with a lower percentage of domestic content threshold than would appear at first sight (for the project to qualify for the domestic content bonus in 2025, 45% of the project’s materials must be sourced in the USA).

Since establishing the domestic content bonus credit as part of the 2022 Inflation Reduction Act, the government has provided multiple rounds of guidance on how to qualify for this incentive.

What is the domestic content bonus tax credit?

The 2022 Inflation Reduction Act established an additional 10 percent tax credit beyond the Investment Tax Credit (ITC) and the Production Tax Credit (PTC) for projects that satisfy requirements for domestically manufactured materials. This tax credit aims to encourage investment into the U.S. supply chain while supporting larger goals for deploying renewable energy, a win-win for manufacturers and solar development in the United States.

In May 2023, the IRS and the Department of the Treasury issued initial guidance for the bonus credit qualification requirements. In addition to satisfying the prevailing wage and apprenticeship requirements from the IRA, a percentage of total manufactured product costs from domestic components (steel, iron, and manufactured products) are required for an energy project to qualify for the bonus credit. This percentage increases over the coming years:

| Commencement of Construction Year | Domestic Content Percentage |

| 2024 | 40% |

| 2025 | 45% |

| 2026 | 50% |

| 2027 and beyond | 55% |

This initial guidance required taxpayers to determine the direct cost (materials and labor) to produce the product and what percentage of those costs came from domestic components. Tracking and documenting sensitive cost details from OEMs for the various structural components that make up a solar or storage project proved to be a detailed and time-consuming process. Often, companies struggled to determine (or convince their finance parties) whether their projects qualified for the requirements and may have missed out on taking advantage of this bonus credit.

Simplified elective safe harbor domestic content calculations

In May 2024, the government issued new guidance known as the elective safe harbor rule, helping to ease the burden on companies looking to qualify for the domestic content bonus credit. This update simplified the calculation methodology, providing component cost percentages for different types of solar projects (fixed, tracking, rooftop) and energy storage projects (grid-scale and distributed).

Instead of tracking down actual costs from manufacturers to use in domestic content calculations, solar developers can rely on the cost percentages provided by the IRS, adding up the component percentages to determine if a project will meet the total domestic content percentage requirement. Steel or iron used in these projects must be 100% domestically produced for the energy project to qualify as domestic content. Beyond that requirement, the remaining domestic content materials must add up to at least 45% in 2025.

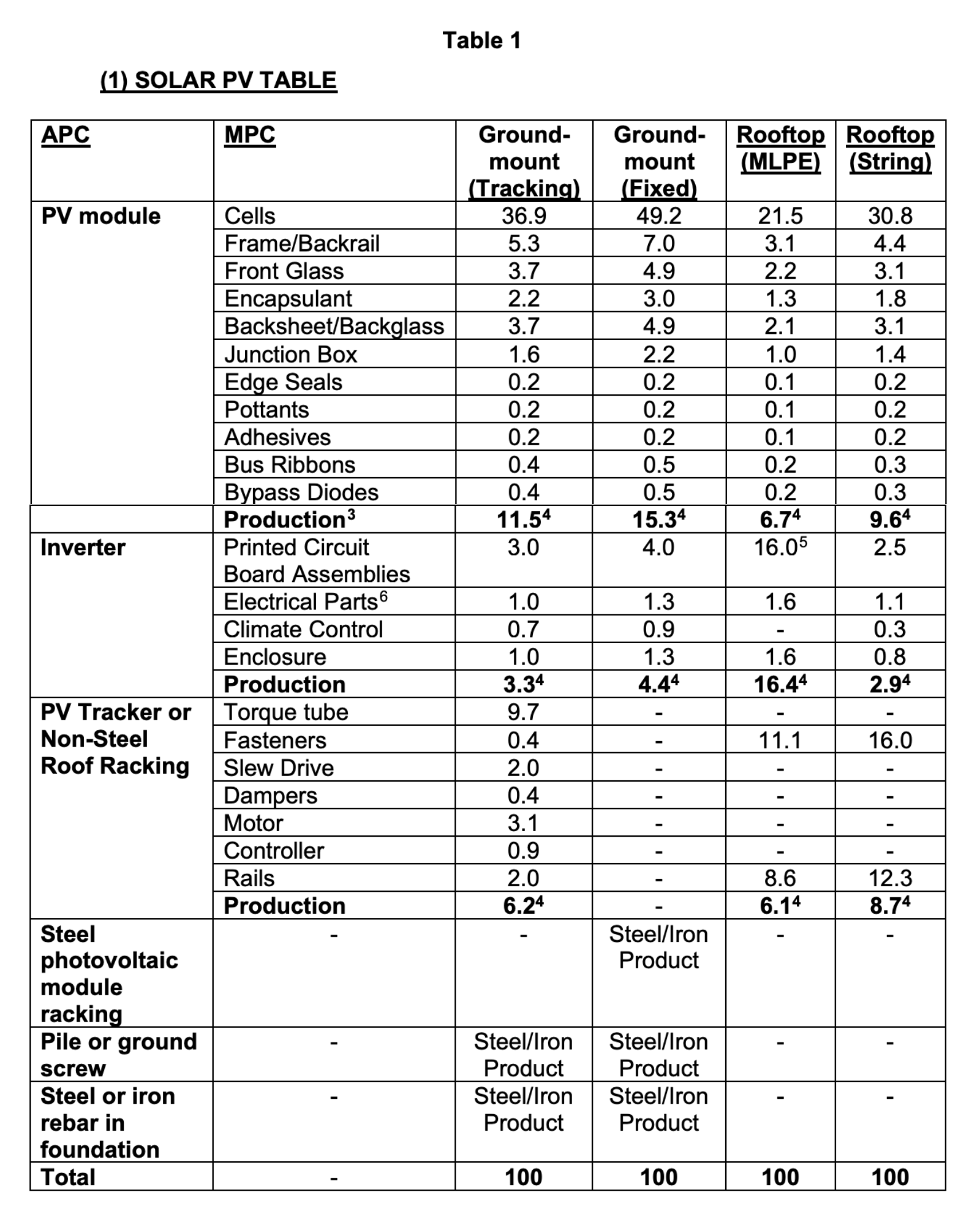

A portion of Table 1—New Elective Safe Harbor provided in the Domestic Content Safe Harbor Notice from the IRS.

Nuances to consider: domestic vs. non-domestic options

While the safe harbor rule and table, which provide a simplified method for determining the percentage of domestic content in a solar project, is a significant improvement from the previous complex and time-consuming direct cost calculations, the process is still not without its challenges. Many solar developers and module buyers may find it difficult to navigate the nuances of domestic content vs non-domestic content options. Determining the right combination of products to qualify for the bonus credit and assessing if the added costs from purchasing domestic content ultimately create more value over the course of the project is a complex task.

As shown in the table above, an additional production percentage is applied if all manufactured product components (MPC) in an assembly (e.g., PV module, inverter, tracker or racking) are domestically produced. As the percentage of domestic content required continues to increase to 45% in 2025 and 50% in 2026, the added production percentage for inverters and/or trackers can make a difference in projects qualifying for the domestic content bonus credit.

Starting in 2025, the proposed technology-neutral ITC and PTC is set to go into effect, allowing for additional technology types to qualify for these clean energy tax incentives. With this change, experts believe each technology (solar, storage, etc.) is considered separately for ITC, PTC, and domestic content. For solar + storage projects, each technology (solar and storage) will need to qualify for the domestic content bonus separately.

The availability of domestic wafers for US domestic content solar panels looks to be limited for years to come as domestic manufacturing ramps up. QCells’ facility in Georgia is the only known domestic wafer manufacturer at this time. If a domestic wafer requirement is added to the final guidance without an extended transitional period before going into effect, the number of solar projects qualifying for domestic content could be drastically limited.

2025 IRS Updates to Domestic Content

The First Updated Elective Safe Harbor (N 2025-08) is issued, modifying the table cost percentages for solar and BESS projects and supplying additional clarifying definitions for project components and manufactured product components for solar PV and BESS. Again, the requirement for 100% U.S.-made steel and iron and the need to satisfy the minimum prevailing wage and apprenticeship standards from the IRA still apply to the First Updated Elective Safe Harbor table. As with other guidance issued, taxpayers can rely on this guidance for projects commencing construction up to 90 days after the release of further guidance.